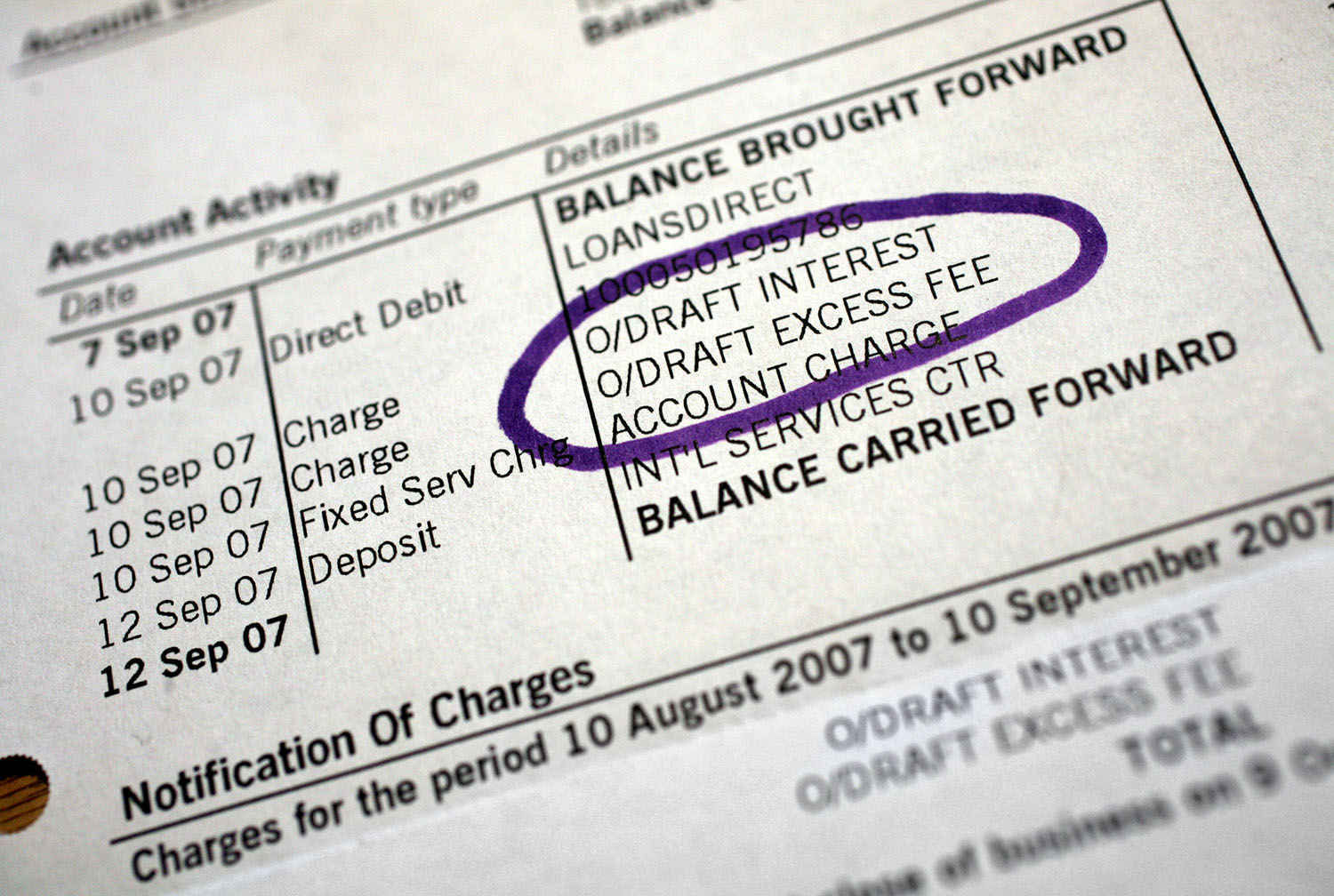

Banks increasingly rely on customer-unfriendly overdraft fees to make up revenue they aren’t getting from loans, according to a new report that will provide another problem for an industry already in trouble over customer service scandals.

Most big banks charge at least $35 each time an overdraft is incurred on a checking account, the Pew Charitable Trusts reported in a study Tuesday. More than 40 percent of banks structure transactions in such a way as to maximize overdraft fees, and 80 percent allow overdrafts on ATM and debit transactions.

Recommended Stories

Banks earned at least $11 billion in overdraft fees in 2015, the report noted. Income from fees and services has grown in recent years as banks have earned less on interest income. “Overdraft has evolved from an occasional courtesy into a product that many banks rely on for revenue,” the report concludes.

The people most likely to pay overdraft fees are lower earners, with the great majority earning less than $50,000 a year. In some cases, customers might intentionally incur overdraft fees, effectively overdrawing their account as a form of expensive short-term credit. For them, bank overdrafts could be an alternative to payday loans, pawning possessions or other forms of emergency credit.

Nick Bourke, the director of Pew’s consumer finance project, said the results suggested that regulations are needed to prevent overdrafts from becoming an expensive form of credit for vulnerable customers. “Regulators should set reasonable limits on overdraft fees and help banks create new small-credit options for those who want them,” he said.

The report’s timing is not good for banks that might want to avoid such regulations. Congress and the public have become more skeptical of banks’ customer service following the revelation of Wells Fargo’s fake accounts scandal, in which bank employees created millions of fake accounts for customers for years to meet sales targets. Those fake accounts resulted in some added fees for customers.

Pew’s report examined the 50 largest banks’ overdraft policies, checking whether they met such preferred practices as refusing debit transactions or ATM withdrawals that would incur overdrafts. Another criterion was whether the bank avoided processing transactions from largest to smallest. Doing so can maximize overdraft fees: The largest charges push the account into deficit, at which point each of the smaller charges counts as a separate overdraft.

The only megabank to meet all of Pew’s recommendations was Citibank. Wells Fargo was dinged for allowing overdrafts on debit transactions and ATM withdrawals.